The other days I discussed with a well-known journalist about the reasons of Viktor Orban`s success in Hungary. My interlocutor was talking admiringly about him because he had understood that Hungary could no longer be underpinned by a foreign direct investment model and that Romania should follow suit.

He argued that foreign capital flows leaving the country were larger than those going in, which meant that the state was being stripped by foreign investors. Moreover, he was suggesting that Romania should follow Hungary`s example and base its growth on local capital exclusively as the only way to elude the “middle-income trap”. Continue to rely on foreign investments and we would never get out and the numerous countries that never succeeded in doing so was evidence enough.

This is a way of thinking that seems to be shared by enough people to warrant a comment on my part. All the more so as I deeply disagree.

Firstly, when putting capital flows in one basket as done above it is similar to comparing apples and oranges. On the one hand, foreign investment income in Romania, dividends in particular, is compared with foreign direct investments (FDI) that is with capital injections. That income is recognized in the Current Account of the Balance of Payments, whereas FDI is entered into the Capital and Financial Account. The very difference in the Balance of Payments recognition suggests that they are two separate things.

Investment income reflects the return on capital invested in Romania. I do not believe that an investor should bring in capital on a permanent basis to justify his/her dividend payment. At the end of the day, the bank does not require us to keep increasing our deposits to get an interest rate and no public firm makes dividend payments conditional on continuing to buy shares. I do not believe that anybody imagines that an investor, local or foreign, is a charitable organization. They invest capital to obtain revenue from that investment, and, Yes, in the end revenues must exceed the amount invested. Therefore they will repatriate more than they have invested. Otherwise they would not have decided to invest in the first place. It is highly likely that, at some point, the investment ceases to grow and yet still generate income. There is nothing abnormal about that.

At the same time, with such a timid presence of Romanian companies abroad, dividends exiting Romania are expected to be significantly larger than those coming in. Is it desirable to have the imbalance corrected by capital inflows? Yes, but this is not an easy task because it all depends on the opportunities provided by the country in question. It is not realistic to expect capital inflows from investors already operating here. Because they have a business plan which requires them to eventually recoup the initial investment. The answer is to draw year on year more new investors to create foreign capital inflows. And that cannot be done using a hostile rhetoric to foreign investments…

Growth based on local capital? What capital are we talking about, I asked my interlocutor. “Well, what about the bank deposits?” he answered. As if the whole economy could be funded through lending. As if banks do not require companies to have a sound equity capital to grant loans. In a decapitalized country such as Romania it is a joke to assume that catching up with the rest of Europe can be currently funded mainly by domestic capital. Even though there is a vehicle that produces the fastest domestic capital growth ever to be seen in Romania. Yes, this is the private pensions system. So I would say that this is one of the main reasons why we should keep and help it grow at least equally fast, if we dream of growth driven by domestic capital.

Do foreign capital inflows have anything to do with the middle-income trap? Hardly. And not because foreign companies were one of the few major factors that contributed to productivity growth and eventually to wage increases..

The reasons are linked to having exhausted all the easy ways for a country to achieve growth and development and an inability to switch to a comprehensive development strategy. A study in May 2016 by Professor Pierre-Richard Agenor at the University of Manchester lists the common features of countries stuck in the middle-income trap: decreasing returns on capital, depleted supply of low-cost labor, inadequate protection of intellectual property (which hampers innovation), distorted incentives and a misallocation of talent, no access to advanced infrastructure, no access to funding, and in particular to venture capital.

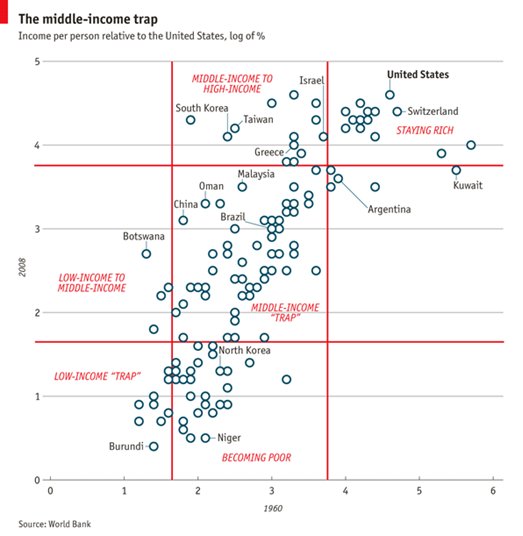

It seems that plenty of governments fail in the process since, as pictured in the chart, extremely few managed to escape the middle-income trap. It is not by chance that among the few countries to have done so were South Korean and Israel, countries that are set apart by innovation and local high-skill intensive industries. I do believe that therein also lies the answer for Romania: a local financial capital shortage can be offset by making the most of the skills available and by a strong infrastructure development. That, however, implies the existence of a driving effect generated by foreign investments, that we will be able to use to our advantage only in so far as the Romanian government and business people can become more efficient and set more ambitious goals.

It seems that plenty of governments fail in the process since, as pictured in the chart, extremely few managed to escape the middle-income trap. It is not by chance that among the few countries to have done so were South Korean and Israel, countries that are set apart by innovation and local high-skill intensive industries. I do believe that therein also lies the answer for Romania: a local financial capital shortage can be offset by making the most of the skills available and by a strong infrastructure development. That, however, implies the existence of a driving effect generated by foreign investments, that we will be able to use to our advantage only in so far as the Romanian government and business people can become more efficient and set more ambitious goals.

As long as that does not happens systemically and systematically, Romania will not be able to get out of the middle-income trap. And to punish foreign investors is similar to beating a pulling horse to death, convinced that you will be able to pull the cart on your own.

As for importing the Hungarian model here, foreign investments per capita in Hungary are five times higher than in Romania. Let us first get there and then we will be able to afford the hypocrisy of complaining of the wrongs they have inflicted on us.

Have a nice weekend!

Subscribe to receive notifications when new articles are published