These comments are designed for those who insist on regularly reassuring us that there are no reasons for concern, that excessively loading the budget with irreversible expenses, such as pensions and wages is sustainable because there is no crisis looming.

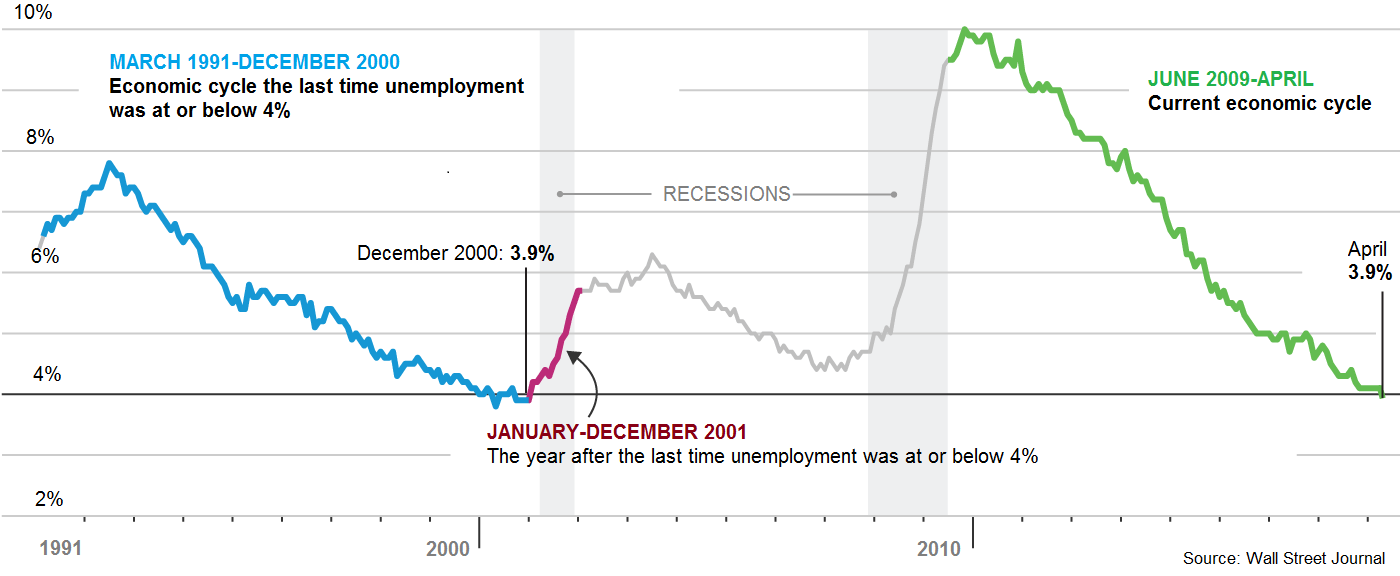

Actually, there have been warning signs which come from several areas. For the purpose of today`s comment I suggest three: the US, Italy and the emerging markets. Firstly, what the US economy demonstrates to us in Romania, still mesmerized by the snapshot image, is how important is to look at the economy in its dynamics. Because there is good news and bad news from the US. The good news is that unemployment is down to 3.9%, an unprecedented low since 2000. A reason for any politician to pat themselves on the back, whether in the US or Romania.

Now comes the bad news, presented by the Wall Street Journal in the graph below. In the past 20 years, each time unemployment decreased by that much, the US economy entered a recession.

The difference, however, seems to be the puzzlingly slow rate of wage increases and the fact that lower inflationary pressures cause interest rates to stay below those in previous occasions. Even under these circumstances, however, it is clear that the moment of truth is drawing near. Even though not as we speak. A Wall Street Journal survey shows that 59% of the interviewed economists see the current growth of the US economy coming to a halt in 2020. From this perspective there are concerns that such a denouement could be hastened by the FED possibly increasing rates too fast. The risk resides in an inverted yield curve of government securities whereby short-term rates could exceed long-term rates. Traditionally such an inversion was interpreted by markets as a sign of coming recession.

The upward trend of interest rates in the US leads to a second category of developments that generate concern: the emerging countries. As many of them have borrowed in dollars when interest rates were lowest, now they find themselves in the situation where their financing costs are bound to increase. Rising interest rates in the US will lead to the dollars leaving the emerging countries and returning to the US. Well-known economists, such as Carmen Reinhart and Paul Krugman distinguish similar signs to those preceding the 2008 crisis or even the 1990 Asian crisis, the latter hitting mainly the emerging economies.

Right now, however, it seems unlikely that the fuse will be lit in Asia. The spark may rather appear in Argentina or Turkey, countries with significant amounts of debt. The populist excesses of the Turkish president who is overtly meddling in the monetary policy of Turkey`s Central Bank only make matters worse by rattling investors.

The second category of risk includes countries such as Indonesia and Brazil, also seriously indebted. A separate category is made up by countries such as the Philippines, India with huge current account deficits and in need of constant foreign currency inflows to fund them. At last, countries like South Africa and Russia could take a serious hit if foreign investor sentiment would turn as investors hold a significant part of the countries` foreign debt.

A third development that we need to keep a close eye on is Italy where two eurosceptic parties, M5S and the League, won the most seats in Parliament. It is worth mentioning that the two parties did not only declare themselves to be against deeper EU integration, but also in favor of Italy leaving the Eurozone. The Italian president`s decision to appoint a technocrat instead of the nominee of the parliamentary majority will probably throw Italy into a political crisis to end up in early general elections.

Many analysts foresee a radicalization of the electoral campaign which may turn into a covert referendum on Italy staying in the Eurozone. People`s financial frustrations feed the rise of populist parties as Italy`s economy shrank by 5% compared to 2001, and youth unemployment stands at over 30%.

Financial markets are watching unnerved the developments in Italy. Interest rates on Italian bonds are increasing even though they continue to remain low, while investors opt for safer investments, such as the dollar and the US Treasuries whose value is rising. Keeping in mind the growing investor nervousness, the Fed may think twice before increasing the rate in June as many expect.

With a public debt at 130%, Italy is twice as indebted as a country such as Germany. Moreover, Italian banks have a larger exposure to local bonds than any other Eurozone bank. That means that the chances that a possible restructuring of the Italian public debt could cause the Italian financial system to collapse are high.

The reaction to the political crisis as regards the Italian two-year bonds was immediate as they saw the biggest one-day jump in the last 26 years. Moody’s announced a downgrading of Italy`s rating if the elected government fails to find ways to decrease the public debt burden. The spillover of concerns related to Italy into the Spanish and Portuguese government securities markets shows the route that an Italian crisis could take to spread across the entire European economy and beyond. Concerns relating to the future of the Eurozone caused the US index, Dow Jones, to lose 400 points in one day while the US two-year Treasury bond yield (their price increase) dropped at the same time in what was the highest one-day fluctuation in the last two years.

These are the three economic areas of risks which must be monitored, although nobody sees the prospect of a crisis in the short-term. The reality, however, demonstrates that nobody is a prophet in their own country. Early 2008, a high-profile and well-informed person in Romania, a long-lasting manager of a financial institution essential in any country was stating that “I see seven more years of economic growth”, with a 7% fall to occur the following year.

Have a nice weekend!

Subscribe to receive notifications when new articles are published