Some pundits or opinion leaders` temptation to estimate the future by looking at historical changes does not cease to amaze me. It is the clear proof that we are still in the dark as to what we are going through, we fail to understand that as witnesses and subjects to a total paradigm shift we have entered unchartered waters. And History will do little to help.

A good example in that sense is the current apparent lack of linkage between the labor market and wage trends. Until recently the link could be explained theoretically and was demonstrated on many occasions throughout the economic developments of the modern human society. And it went as follows: as the economy recovers, the unemployment rate starts to fall, and as the available workforce pool decreases, the average wage increases. The scarcer a commodity, labor in our case, the more expensive it gets. It does make sense, doesn`t it?

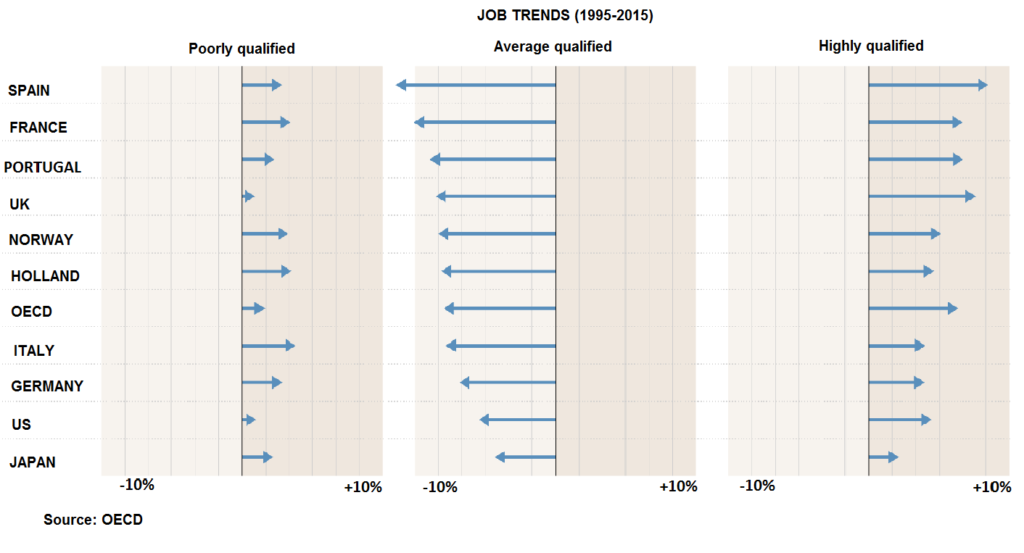

It appears that this logic stopped working. Most developed economies present the same signs, with the US drawing the spotlight. Resuming hiring does no longer lead or it does but to a small extent to an average wage growth. There is a disconnect somewhere. The explanation seems to lie in the disruptions brought about by the digital revolution. The chart below, based on OECD data, shows the labor market changes over the last 20 years in a number of developed countries.

Overall the trend is clear: there are fewer jobs that require medium skills and more jobs requiring low and high-skilled workers. This process will only be stepped up in the coming period as artificial intelligence will replace medium-skilled jobs in particular. A trend, however, which will cause the average wage, and I underline average, not to experience any major changes.

The lack of wage growth presents central banks with a serious conundrum. Without rises in pay the economy and prices cannot increase. And if prices stagnate, there is no inflation. With no inflation and accelerated growth, central banks have no reason to increase interest rates. This is exactly the debate going on in the US on the attitude that the FED show adopt with regards to the interest rate policy as neither wages, nor inflation have increased.

On the other hand, the central banks in the US, Eurozone and Japan have printed and flooded the market with vast amounts of money. They practically created a situation unprecedented in the history of the world`s economy, whose consequences are hard to foresee. That takes us to the next question whose answer we can only guess.

On the other hand, the central banks in the US, Eurozone and Japan have printed and flooded the market with vast amounts of money. They practically created a situation unprecedented in the history of the world`s economy, whose consequences are hard to foresee. That takes us to the next question whose answer we can only guess.

With so much money injected into the economy, if it cannot be found in wage rises, or in inflation, where can it be found? The answer is this: if the money is not reflected in consumer goods prices, it can only be found in the prices of other goods, especially goods you can invest in: shares, bonds, real estate, commodities and so on.

This reasoning can have a behavior explanation as well. As polarization increases, as the professional and financial elite rises in both numbers and wealth, their consumption cannot keep up. Their food, clothes, cars, trips reached a plateau and will continue to stay there for the time being. Under these circumstances, the remaining unused income will have to be parked in assets meant to increase its value. And these can be found on the capital market, the real estate and the commodity market. As I was saying, central bank interest rates will continue to remain completely dissuasive given the law inflation rate.

That makes me conclude that financial markets stand a good chance to enter a huge bubble. A bubble which continues to inflate as long as the cash surplus remains on the market and the central banks drag their feet on taking it out of the economy. The banks seem to be currently caught in the bubble effect they created and are afraid that a money withdrawal could cause an avalanche of financial market collapses. Markets will continue to increase for a while, investors will be afraid to go against the tide, but at some point someone will recognize the “naked emperor” and it will all come tumbling down. The amounts lost will be the money withdrawals that central banks hesitated to perform.

As a comparison Romania seems to be featuring in another movie, isn`t it? Or maybe not …

Indeed, wages in Romania are growing consistently, on the back of generous pay rises in the public sector. On the face of it this seems to be making a lot of sense. At the end of the day, why is it so bad for the Romanian government to stay clear of the wage gap already present in other countries?

The bad news is that the Romanian government through its wage policy causes labor market distortions. Unlike the private sector, it does not seem concerned with paying highly qualified professionals, and mass wage growth has nothing to do with any performance criterion. The consequence is massive migration of physicians and a dodgy education system while the private sector managed to stop IT experts from leaving the country and is about to put the brakes on healthcare staff migration and even bring back physicians trained abroad.

The wage euphoria led to a borrowing binge. More money thrown on consumption creating the illusion of a wealth which Romanians are so eager to get their hands on fast.

Even though the Romanian Central Bank did not print money like other central banks, the massive public wage spike at the expense of investments and the multiplying effect of lending for consumption are starting to kick in. The current account deficit puts pressure on exchange rates, while inflationary pressures will force the RCB to increase its interest rate. Budget policies will have to be reversed as they will no longer be sustainable. At the end of the day they will prick the bubble. The bubble of unrealistic expectations.

Have a nice weekend!

Subscribe to receive notifications when new articles are published